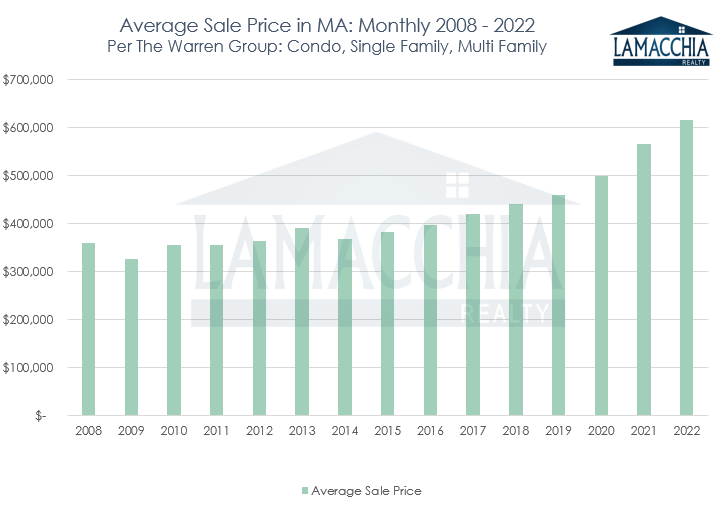

The 2022 Massachusetts Year in Review Housing Report breaks down average prices, sales, inventory, new active listings, and pending sales for 2022 compared to 2021 and illustrates what that means for the current market.

prices, sales, inventory, new active listings, and pending sales for 2022 compared to 2021 and illustrates what that means for the current market.

2022 was another historic year in a succession of historic years for the real estate industry. 2020 the world was rocked by the breakout of COVID, the second half of 2020 and then 2021 experienced a frenzied housing market with inventory lower than it ever has been in recorded history, and 2022 was the tipping point when the market began its journey back to baseline. Market adjustments, global pandemics, and anemic inventory are not for the faint of heart. To have skin in the game of real estate over the past three years has required dedication and resilience and so we are well prepared for what’s to come as we adjust back into a more balanced market.

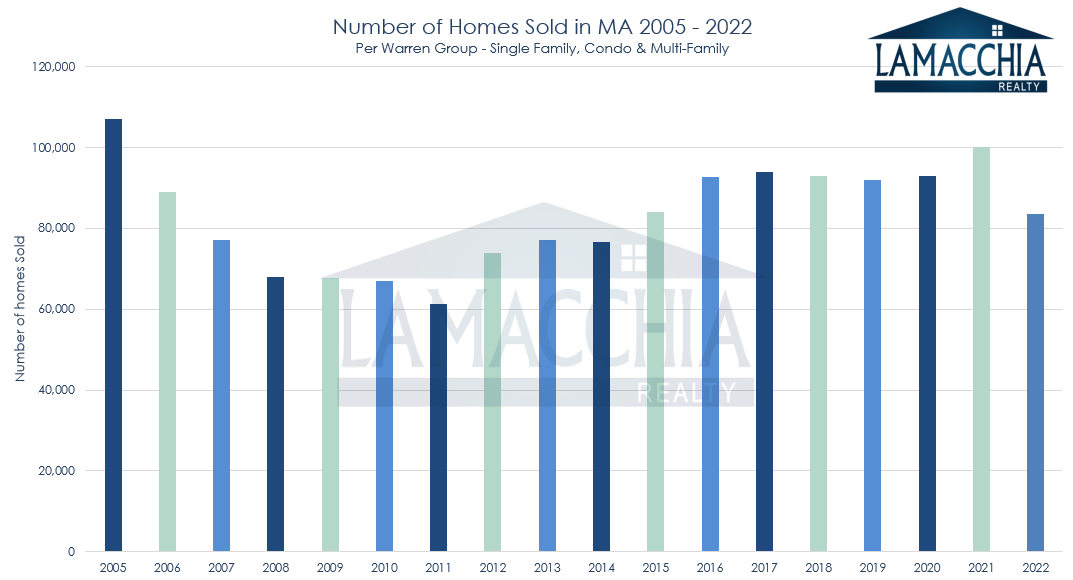

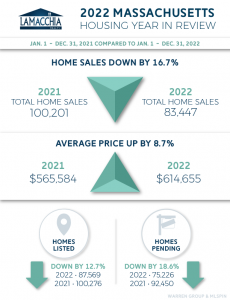

Annual sales for the state of Massachusetts were down for the year. This is NOT a sign that the market is crashing in the typical terms that it is understood. Many twists and turns over the past few years have been easily spun as harbingers of doom for the market- headline-grabbing click-bait. But with everything that’s happened, nothing has crashed yet. Yes, sales are down over 16%, but of course, they are. If you look at the fact that they were down every month this year compared to last, that’s the first clue, but if you look at the rapid and unsustainable rise in sales in 2021 it’s no wonder that 2022 was down. And thank goodness it is. This state (nor does this country for that matter on a grander scale) doesn’t have the inventory available to maintain that level of demand.

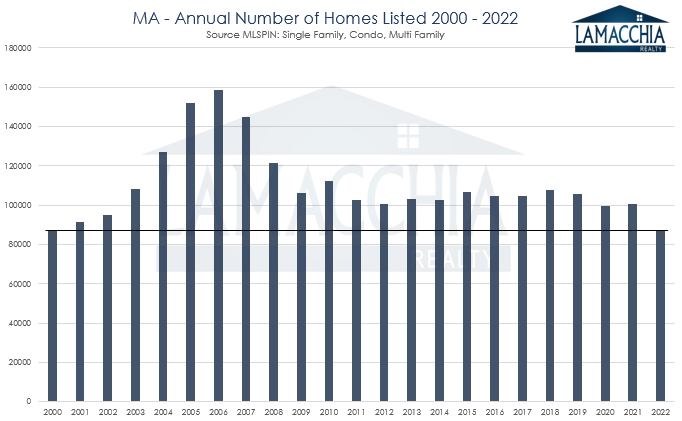

Below is a graph that illustrates home sales per year since 2005. You can see 2021 exhibited an outlying rise in sales, and 2022 exhibited a significant decrease.