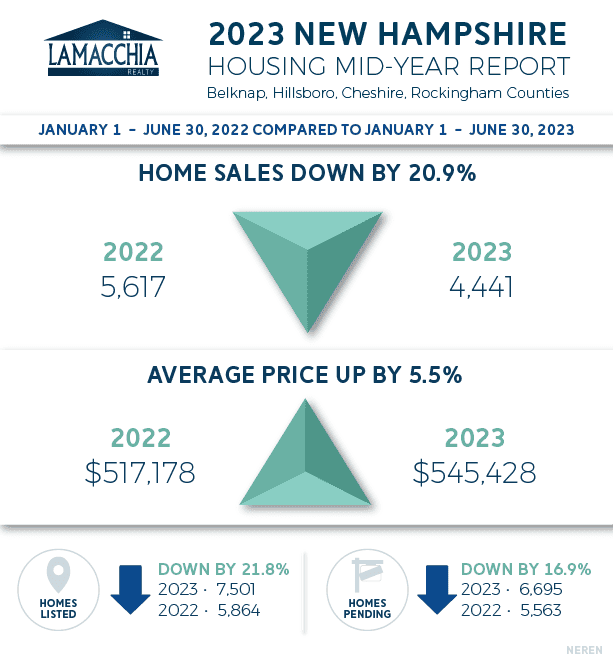

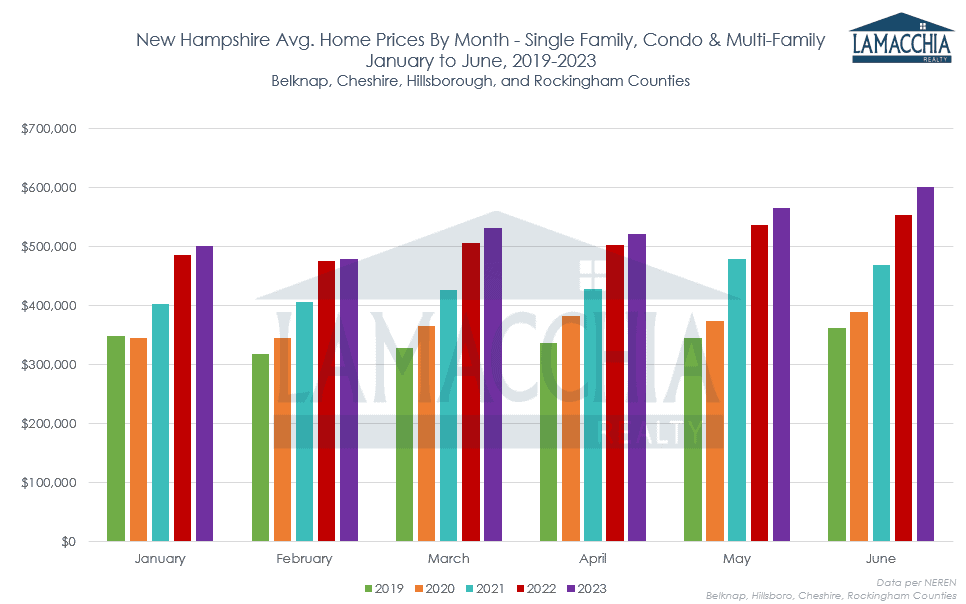

Consistent with New England trends, Belknap, Cheshire, Hillsborough, and Rockingham counties have exhibited a decrease in sales and an increase in prices. This is unfolding as predicted but is causing strain on inventory.

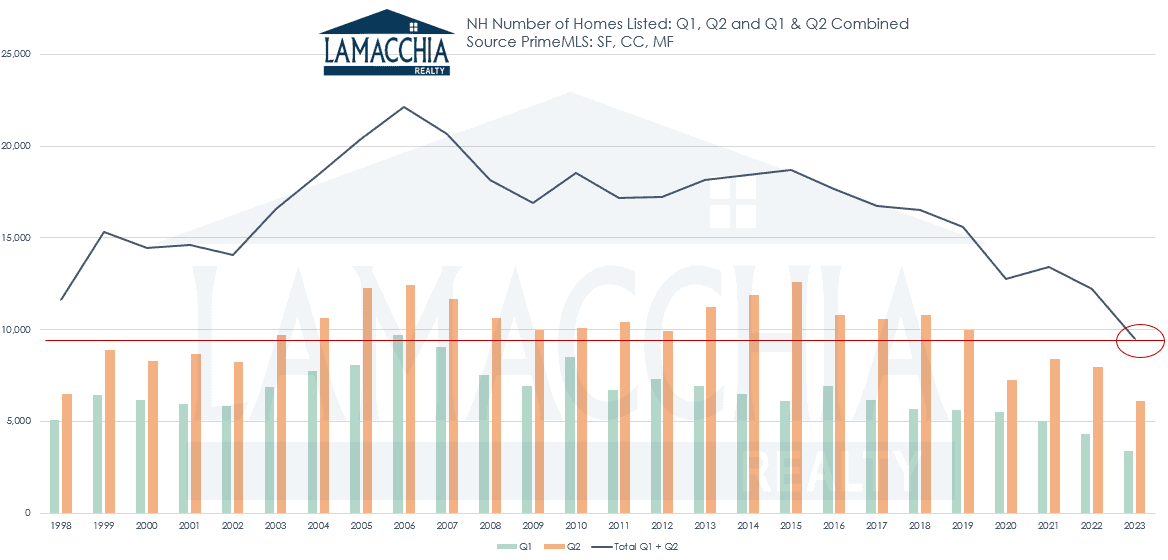

Sellers are hesitating to list due to their Covid-era low rates as trading them in for a more current rate of around 7% is a tough pill to swallow. We predict they will stay at this level for at least the next few months. We also expect that we are going to finish the year with the least amount of homes listed in recorded history.

It has been coming down to necessity and life changes to make sellers list. Circumstances of divorce, family growth, relocations, and downsizing have propelled the market but not enough to raise inventory to meet buyer demand. This is why prices haven’t fallen.

Buyers who are out there are committed to finding the home they want that has what they need within their budget which is lower now compared to last year. Rising rates and prices have decreased affordability but that is why staying on top of rates and pre-approvals is essential. As soon as a rate drop happens, buyers should be getting their preapprovals updated to be ready to strike.

As we enter the second half of the year, sellers are met with a mix of positive and negative market conditions. Historically, the beginning of the year proves to be more of the seller’s market. For those that are selling and buying at the same time, however, the latter half of the year is usually the buyer’s market, so it’s still opportune to list now. To achieve success in this market, competitive pricing for your home is crucial. Drawing in a higher number of potential buyers grants you increased bargaining power, enabling you to have greater control over negotiation terms such as timing, contingencies, and price.

With inventory low and prices still holding tight, a housing crash in prices isn’t on the radar. Though rates are up much higher than the pandemic, historically they’re not that high and it’s a common belief that once the dust settles, 5-6% rates will be the norm. If sellers look at it that way, selling and getting into that new home shouldn’t wait because time isn’t going to bring rates down that much. And if they do and prices are still holding strong, a refinance would be a great option to lock in a lower rate.